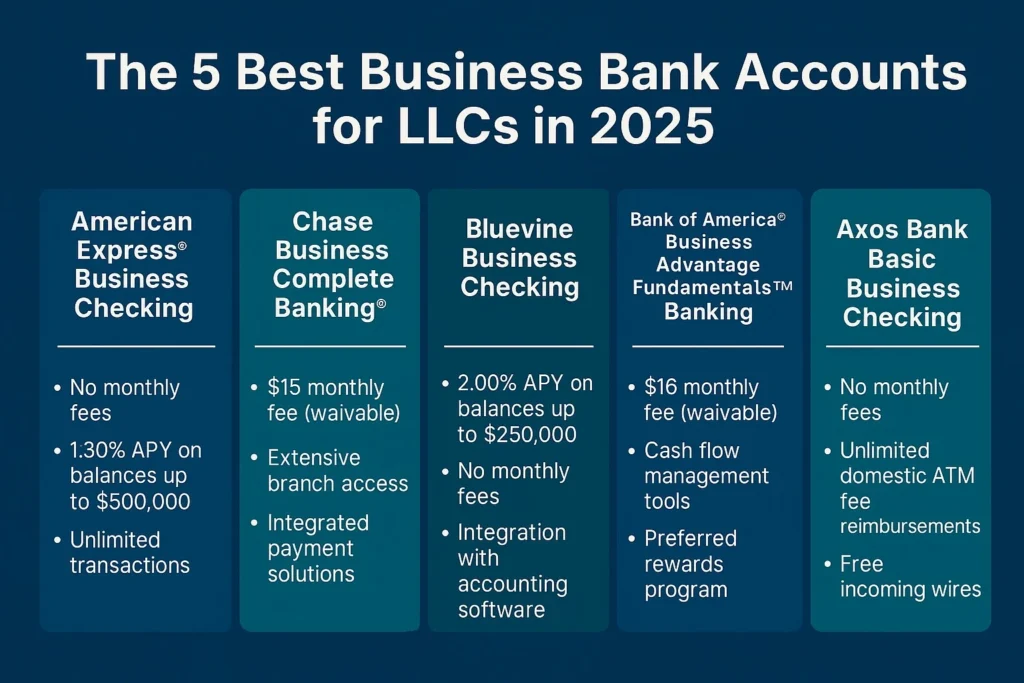

Best Business Checking Accounts for Small Businesses

Picking the right bank account sounds simple until you start comparing fees, transaction caps, cash deposit rules, and online tools. That is where many owners get stuck. The best business checking accounts can save your company real money, but a bad fit can quietly drain cash each month and make bookkeeping harder than it needs to be. If you run a side hustle, a local shop, or a growing service business, this choice matters now because banks keep changing terms, adding digital features, and splitting products by business size. Look past the glossy sign-up pitch. What matters is whether an account matches how your business actually gets paid, spends, and moves money day to day.

What deserves your attention

- Monthly fees are only the start. Transaction limits, cash deposit caps, and wire costs can sting more.

- The best business checking accounts depend on your model. A freelancer needs something different from a retailer handling cash.

- Online banks often win on price. Traditional banks can still make sense if you need branches or in-person deposits.

- Integrations matter. Solid links to QuickBooks, payment tools, and bill pay can cut admin time.

How to judge the best business checking accounts

Start with your workflow, not the bank’s marketing. How many payments hit the account each month? Do you deposit cash? Need same-day ACH, remote check deposit, or outgoing wires?

Here are the big filters I would use after years of watching banks hide the real costs in the fine print.

- Monthly maintenance fee

Some accounts waive it with a minimum balance. Others skip it entirely. That sounds minor, but over a year even a $15 fee adds up. - Transaction limits

Many business checking accounts cap free transactions each month. Go over, and you may pay per item. That model punishes active businesses fast. - Cash deposit rules

If your business handles bills and coins, this is non-negotiable. A low-fee digital account can turn into a headache if cash deposits are clunky or costly. - ATM and branch access

Plenty of owners say they do everything online. Then a problem hits, and suddenly a branch sounds pretty useful. - Digital tools

Look for mobile deposit, account alerts, user permissions, accounting integrations, and clean bill-pay features. - Scalability

The right account today may be wrong six months from now. Think ahead a little.

Business checking is like choosing a kitchen for a busy restaurant. Fancy finishes do not matter much if the layout slows down the staff.

Best business checking accounts by business type

For freelancers and solo owners

If you send invoices, get paid electronically, and rarely touch cash, online-first accounts tend to offer the best value. You want low or no monthly fees, easy transfers, and simple tax tracking. Bells and whistles matter less than clean execution.

Look, this is where many traditional banks lose me. They still charge for basic activity that should be standard in 2025.

For local stores and restaurants

Cash changes everything. A strong business checking account for a retail or food business needs practical branch access, reasonable cash deposit allowances, and merchant services that do not feel bolted on as an afterthought.

Ask a blunt question: how much cash can you deposit each month before fees kick in? If the answer is buried three pages deep, that tells you something.

For growing small businesses

Growth adds friction. More payments, more staff access, more vendors, more reporting. You may need multiple sub-accounts, user controls, stronger fraud protection, and smoother links to payroll or bookkeeping software.

This is usually the point where “free” stops being the best deal.

Best business checking accounts at online banks vs traditional banks

Why online banks often look better on paper

Online providers usually compete hard on price. Lower overhead often means lower fees, fewer minimum balance rules, and cleaner mobile tools. For remote businesses, consultants, agencies, and ecommerce sellers, that can be a strong match.

And yet, there is a catch. Some online accounts rely on partner networks for cash deposits or customer support, which can feel awkward when a real issue pops up.

Why traditional banks still have an edge

Branch access is still useful, especially for cash-heavy businesses and owners who want face-to-face support. Large banks may also offer easier paths into merchant services, lending, and treasury tools as the company grows.

Honestly, this is where convenience can beat price. Paying a little more for fewer operational headaches is sometimes the smart move.

Common fees that trip up business owners

The headline monthly fee gets attention because it is easy to understand. The sneaky charges sit elsewhere.

- Excess transaction fees for going beyond monthly limits

- Cash deposit fees after a set dollar threshold

- Outgoing wire fees, especially domestic and international

- ATM fees outside the bank’s network

- Paper statement fees or account research fees

- Overdraft and returned item fees that pile up fast

One pro tip: estimate your busiest month, not your average month. Banks love average behavior because it hides stress points.

How to compare the best business checking accounts without wasting a weekend

Use a short checklist and force each account through the same screen. That keeps flashy promotions from hijacking your decision.

- List your monthly transaction count.

- Estimate cash deposits, if any.

- Note whether you need wires, ACH, bill pay, or multiple users.

- Check the real monthly fee after any waiver rules.

- Review mobile app ratings and support options.

- See whether it connects to your accounting stack.

Then compare the annual cost, not just the opening bonus. A one-time incentive can distract you from a weak account structure.

What Money Crashers gets right about best business checking accounts

The source roundup from Money Crashers is useful because it frames business checking as a fit question, not a one-size-fits-all pick. That is the right lens. Different accounts work for different business models, and owners should compare fees, access, and tools with that in mind.

But here is my pushback. Lists of the best business checking accounts are only helpful if you translate them into your actual operating pattern. A bakery, a web designer, and a contractor may all hate the same account for completely different reasons.

Questions to ask before you open an account

Before you sign anything, ask these directly:

- How many free transactions do I get each month?

- What are the cash deposit limits before fees start?

- Can I send ACH payments and wires from the app?

- Does the account support integrations with QuickBooks or Xero?

- How fast is customer support, and is it phone-based, chat-based, or branch-based?

- What happens if my business outgrows this account?

Why leave those answers to guesswork?

Where I would lean

If your business is digital-first and does little or no cash handling, start with low-fee online options and compare app quality with a skeptical eye. If you run a local operation with steady cash deposits, branch access and deposit terms should carry more weight than a “free” label.

The best business checking accounts are the ones that fade into the background because they fit your operation cleanly. Compare three serious options, read the fee schedule line by line, and pick the account that will still make sense after your next growth spurt.