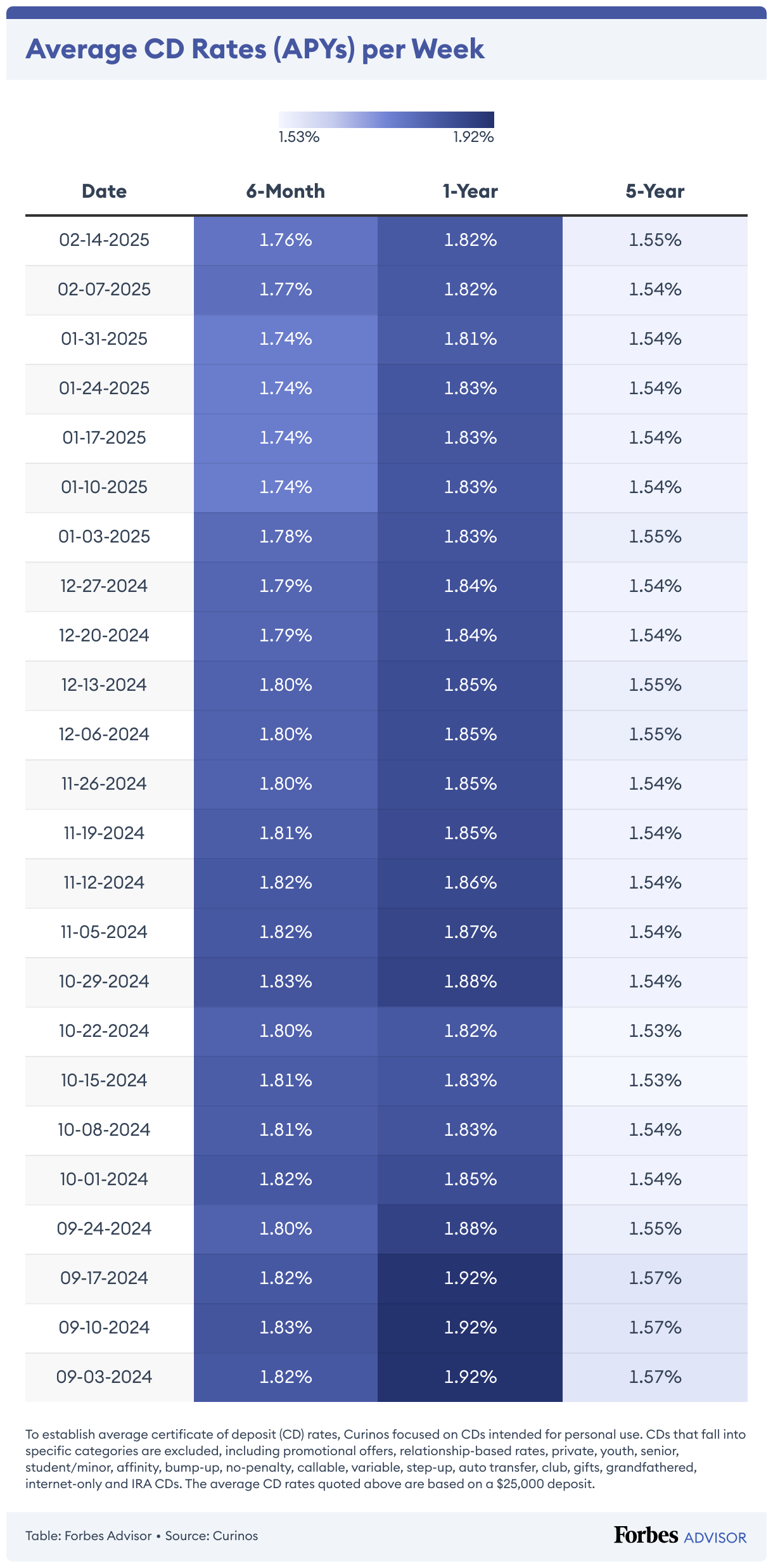

Best CD Rates Right Now: Earn More Without Guesswork

You want savings that pay real yield without turning into a second job, and the hunt for the best CD rates feels urgent because Treasury moves keep reshaping bank offers overnight. Rate tables look similar, but small differences in term length, early withdrawal penalties, and account minimums decide how much you actually keep. The short list below cuts through marketing fluff so you can grab high APYs, time your ladder, and dodge fees. Why let your cash idle when it can earn predictable returns?

Quick Wins With Top Rates

- Short terms (6-12 months) often beat longer CDs when the Fed pauses, so check current yield curves.

- Online banks with no branch overhead usually post the highest APYs and lower minimums.

- Early withdrawal penalties can erase gains; pick terms you can hold.

- FDIC or NCUA insurance up to limits keeps principal protected.

- Laddering CDs smooths rate risk and restores cash flow.

Why the Best CD Rates Matter

High-yield CDs beat standard savings by a wide margin, especially when promo offers stack with loyalty bumps. Banks use CDs to lock funding, so they price aggressively when deposit competition heats up. Think of it like a coach setting a batting lineup: put your short-term cash in the leadoff spot with a 6-month CD, while longer cash bats cleanup in a 24-month term.

Spotting Real Top-Tier Offers

- Check APY against term peers, not just headline numbers. A 5.3% six-month CD may outperform a 4.8% two-year CD after penalties.

- Verify minimums. Some credit unions ask for $500, while niche banks demand $10,000.

- Confirm compounding frequency. Daily compounding slightly bumps effective yield.

- Read the penalty math. Two months of interest hurts less than six if you need out early.

Lock a term only as long as you can stomach. Breaking a CD to chase a new rate often backfires.

Building a CD Ladder With the Best CD Rates

Laddering spreads maturity dates so you catch rising yields without freezing all cash. Start with three rungs: 6, 12, and 18 months. As each CD matures, roll it into the longest rung to keep the ladder moving. This rhythm balances yield and access.

Liquidity is your safety net.

If you expect rates to slide, extend the ladder to 24 or 36 months to lock current highs. If you expect hikes, keep rungs short and reinvest quickly. How do you balance yield and flexibility when the market refuses to sit still?

Best CD Rates vs High-Yield Savings

High-yield savings accounts stay liquid, but the APY can drop with no notice. CDs trade flexibility for predictability. If you need quick access for emergencies, keep at least three months of expenses in savings and put surplus cash into CDs. This split acts like a basketball rotation: starters (savings) handle urgent plays, while bench players (CDs) preserve energy and score steadily.

Finding the Best CD Rates at Online Banks

Online banks tend to win on APY thanks to lower overhead and faster rate updates. Scan for banks with strong mobile apps, same-day funding, and clear disclosures. Avoid teaser rates that reset to mediocre yields after one term. And look for member-only credit unions that open nationwide; many post standout CD specials without heavy marketing.

Penalty Traps and How to Avoid Them

Read the early withdrawal fine print. A three-month penalty on a six-month CD can erase most earnings. A six-month penalty on a five-year CD can turn a mid-term exit into a loss. Choose terms you are confident about, and keep an emergency stash elsewhere so you do not break a CD out of panic.

Taxes and Insurance on the Best CD Rates

CD interest is taxable in the year earned, even if you do not withdraw it. Consider putting CDs inside tax-advantaged accounts if available. Confirm FDIC or NCUA coverage and keep balances within insurance limits by splitting deposits across institutions when needed (a simple spreadsheet helps track totals).

Trusted Moves to Act Now

- Set rate alerts with your bank or aggregator to catch new promos fast.

- Fund new CDs early in the morning when same-day ACH windows open.

- Revisit your ladder every quarter to match cash needs and market moves.

- Keep documentation of terms and penalties for each CD.

Where CD Rates Go Next

Short-term rates tend to follow Fed meetings, while long-term CDs shadow Treasury yields. If inflation cools, expect banks to trim offers. If economic data surprises to the upside, promos may return. Stay nimble, but do not wait forever—idle cash earns nothing.

I have covered enough rate cycles to know one thing: decisive savers usually earn more than perfect timers. Grab the yield that fits your plan and adjust when the market gives you a better pitch.