Debt Payoff Plan for Teachers That Actually Works

You have a classroom to run and a stack of bills that keep you up at night. A focused debt payoff plan for teachers respects both realities, and that matters now with rates still punishing anyone who carries balances. You can tame the interest, curb the habit spends, and still keep some joy in the budget. The clock is ticking on compounding charges, but you control the next move.

Quick Wins You Can Use Now

- Freeze all new credit use and move balances to the lowest-rate option available.

- Automate minimums plus a fixed extra payment on the highest-rate card.

- Trim subscriptions and dining to fund that extra payment.

- Build a bare-bones $1,000 emergency fund to avoid new debt.

Why a Debt Payoff Plan for Teachers Beats Winging It

Teaching runs on structure. Your money needs the same rhythm. Without a plan, interest eats raises and stipends before you can enjoy them. With a simple ladder—pay the highest-rate card first while holding minimums elsewhere—you reclaim momentum fast. Think of it like classroom management: consistent rules beat chaotic reactions.

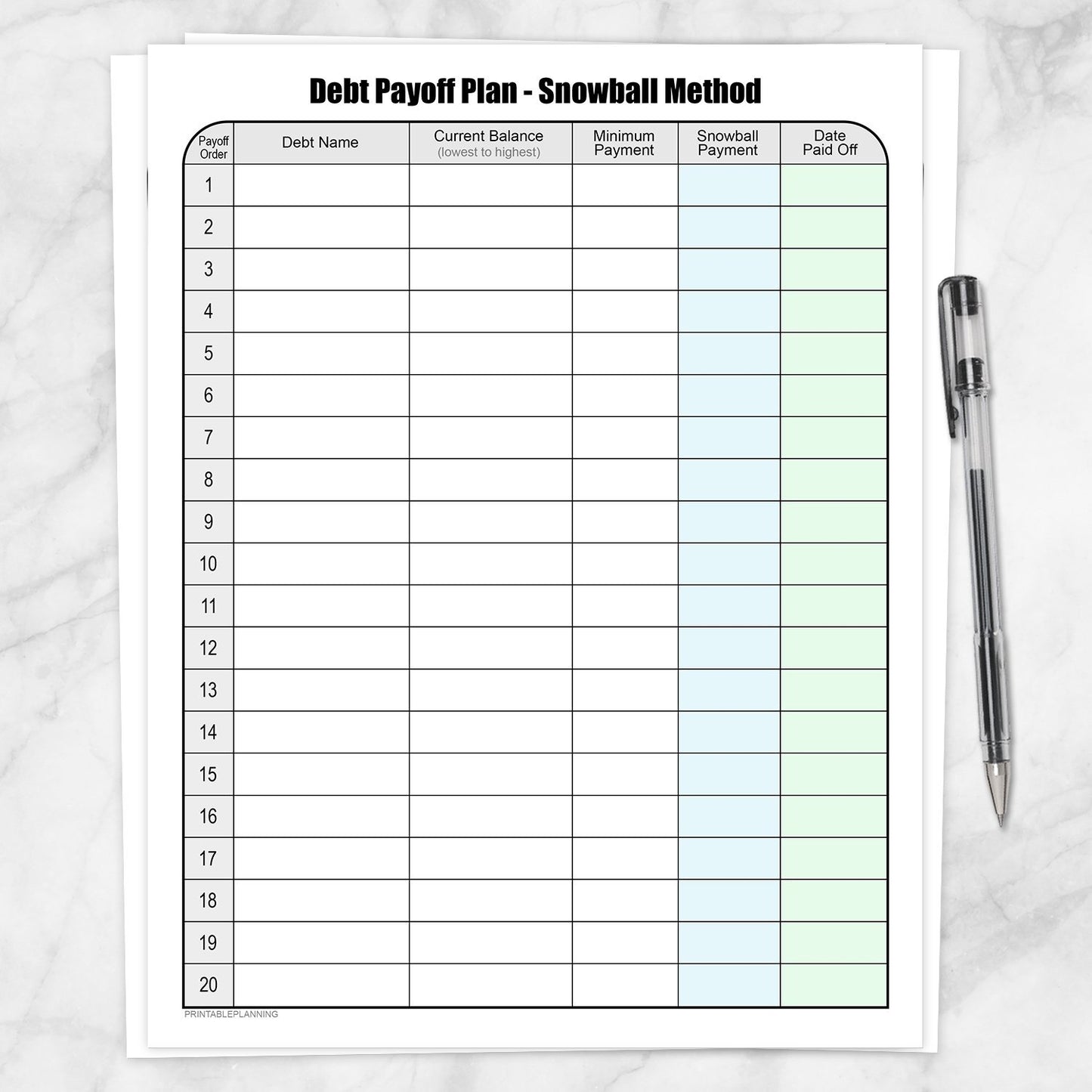

Set the rule once: every extra dollar hits the highest APR balance until it vanishes.

Map the Spending Triggers

Look at last three months of statements. Highlight restaurants, Amazon, and quick convenience buys. Those are the leaks. One single-sentence paragraph exists here.

Cap each leak with a weekly cash envelope or a prepaid card so you feel the spend. But what if you miss out on social time? Rotate hosting at home. It saves cash and keeps connections alive (and you control the menu). Like coaching defense in basketball, the best play is to cut off the passing lanes before the shot even goes up.

Refinance and Consolidate Wisely

If your credit score is decent, check credit union personal loan offers. Aim for a rate below your current cards. But avoid long terms that drag out the pain. Refinance once, close with a clear payoff date, and never reopen the cards until balances are zero. Does a balance transfer fit? Yes, if the fee is smaller than three months of interest and you can clear the promo before it expires.

Boost Income Without Burning Out

Extra income accelerates every payoff chart. Still, burnout is real. Try district stipends for coaching, tutoring, or summer school before hunting outside gigs. Hourly work at a test-prep center can deliver high pay per hour without lesson planning. Sell unused gadgets and teaching materials you no longer need. Every dollar gets routed to the top APR balance.

Protect the Basics While You Pay Down

Emergency fund first. Then retirement match if available—skipping free money is a self-inflicted setback. After that, all surplus attacks debt. Keep renter’s or homeowner coverage active; one mishap can shove you backward. And track progress monthly so you see the slope changing.

Money Habits That Stick

- Set a weekly money check-in every Sunday night.

- Use one checking account for bills and one for spending to avoid mixing funds.

- Automate transfers on payday so choices shrink.

- Celebrate debt payoff milestones with free rewards like a park day or library movie night.

Closing Thoughts on Your Debt Payoff Plan for Teachers

Look, compounding interest is a relentless opponent. But your schedule, your plan, and your habits can outwork it. Keep the play simple, move the ball every week, and ask yourself: how good will it feel to cash your paycheck and know none of it vanishes to old debt? Start now, because a year from today you will either be lighter or still waiting.