Debt Snowball vs Avalanche: Which Payoff Method Fits You?

If you are staring at multiple balances and wondering where your extra payment should go, the debt snowball vs avalanche debate matters right now. The method you choose can change how fast you get out of debt, how much interest you pay, and whether you stick with the plan long enough to finish it. That last part gets ignored too often. People love clean math, but debt payoff is also about behavior, stress, and momentum.

I have covered personal finance long enough to know this: the “best” method on paper is useless if you quit after two months. You need a system that works in real life, with uneven paychecks, surprise bills, and the mental drag that debt creates. So let’s sort out what each method does, where each shines, and how you can choose without overthinking it.

What matters most

- Debt avalanche usually saves more money because it targets the highest interest rate first.

- Debt snowball usually feels easier to sustain because it targets the smallest balance first.

- If motivation is your weak spot, snowball can beat avalanche simply because you keep going.

- If your rates are steep, avalanche deserves a hard look because the interest damage adds up fast.

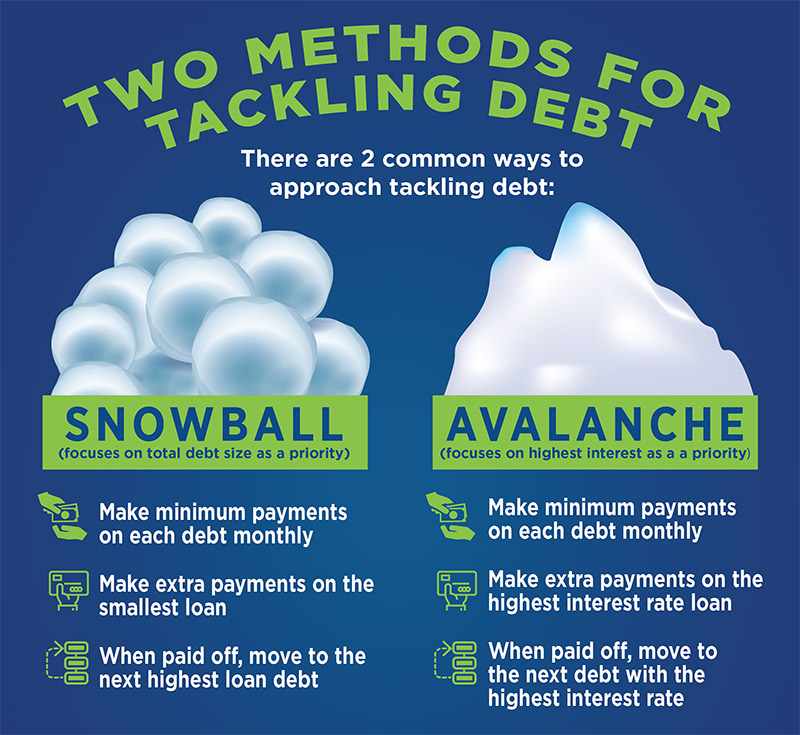

What is the debt snowball vs avalanche difference?

Both methods ask you to make minimum payments on every debt, then throw any extra cash at one target balance.

The split is simple:

- Debt snowball: Pay off the smallest balance first, no matter the interest rate. Then roll that payment into the next smallest balance.

- Debt avalanche: Pay off the highest interest rate first, no matter the balance size. Then roll that payment into the next highest rate.

Think of it like cleaning a messy garage. Snowball clears the small boxes first so you see progress. Avalanche starts with the heaviest junk because it causes the most trouble.

Same idea. Different psychology.

Why the debt avalanche usually wins on math

If your goal is to pay the least interest possible, avalanche is usually the stronger move. By attacking the highest APR first, you cut the costliest debt before it keeps compounding against you.

Say you have these debts:

- Credit card A: $2,000 at 29% APR

- Credit card B: $900 at 18% APR

- Personal loan: $5,000 at 11% APR

With avalanche, credit card A gets your extra payment first because 29% is brutal. With snowball, credit card B goes first because $900 is the smallest balance. Which saves more? In most cases, avalanche. The gap may be modest or pretty wide, depending on balances and rates.

High-interest debt is the leak in the boat. You can admire small wins, but you still need to plug the biggest hole.

And if you are dealing with store cards or credit cards above 25% APR, this is not a small detail. It is expensive.

Why the debt snowball works for so many people

Personal finance people sometimes sneer at snowball because it is not the pure math answer. Honestly, that misses the point. Humans are not spreadsheets.

Snowball gives you a faster early win. One balance disappears. Then another. That visible progress can lower stress and build confidence, especially if you have been avoiding your debt numbers for months.

This is the method popularized by Dave Ramsey, and the appeal is easy to see. Early victories create momentum. For plenty of households, that momentum is non-negotiable because the toughest part is not choosing a formula. It is staying engaged.

Debt snowball vs avalanche: which method should you choose?

Ask yourself one blunt question: are you more likely to quit from slow progress, or from seeing too much interest pile up?

Pick debt snowball if:

- You need quick wins to stay motivated.

- You have several small balances you can knock out fast.

- You feel overwhelmed and need a simpler starting point.

- Your interest rates are fairly close together.

Pick debt avalanche if:

- You want to pay the least total interest.

- You are disciplined enough to wait longer for visible wins.

- You have one or two very high APR debts.

- You track numbers closely and like an efficiency-first plan.

There is no prize for choosing the “smarter” method if it makes you stall.

How to start a debt payoff plan that actually sticks

Look, the method matters less than the system around it. A shaky budget can wreck either approach.

- List every debt, including balance, APR, minimum payment, and due date.

- Build a bare-bones monthly budget so you know your real extra payment amount.

- Set up automatic minimum payments on all debts to avoid late fees.

- Choose snowball or avalanche and target one debt with every extra dollar.

- Keep a small emergency buffer so a car repair does not push you back onto a credit card.

That emergency buffer matters more than many payoff plans admit (even $500 can help). Without it, one surprise expense can blow up weeks of progress.

Can you combine debt snowball vs avalanche?

Yes, and for some people that is the sweet spot.

You might start with snowball to clear one or two tiny balances, then switch to avalanche once you feel traction. Or you might use avalanche for any debt above 20% APR, then snowball the rest. Purists may hate that hybrid approach. Too bad. If it works for your behavior and your budget, it works.

What matters is reducing balances, avoiding new debt, and keeping the process simple enough to repeat every month.

Common mistakes that slow debt payoff

- Ignoring interest rates completely. Snowball is fine, but do not pretend a 30% APR card is harmless.

- Closing old credit accounts too fast. That can affect your credit utilization and average account age.

- Skipping an emergency fund. Then every surprise bill becomes new debt.

- Paying extra without a plan. Random payments feel productive but often waste momentum.

- Forgetting behavior. A payoff plan fails fast if spending habits stay the same.

And here is the bigger issue. If your debt came from a chronic monthly shortfall, no payoff method can fix that by itself.

What experts generally agree on

The Consumer Financial Protection Bureau and major personal finance educators tend to agree on the fundamentals: know your balances, make at least minimum payments on time, reduce high-interest debt, and choose a repayment strategy you can maintain. The disagreement is mostly about emphasis. Math or motivation?

My view is pretty simple. If your debt carries ugly rates, avalanche deserves first consideration. If your biggest risk is giving up, snowball may be the wiser call. The best plan is the one you will still be following six months from now.

Your next move

Pick one method tonight and run the numbers on paper. Then automate it.

If you want the cheapest route, start with avalanche. If you want a plan that feels less punishing, start with snowball. But do not spend three weeks debating labels while interest keeps piling up. Which is worse, choosing an imperfect method, or staying stuck?