Financial Order of Operations: What to Prioritize First

You can make solid money decisions and still feel stuck if your priorities are out of order. That is the real problem with personal finance. You are earning, spending, saving, and paying down debt, but each move pulls in a different direction. The financial order of operations gives you a clear sequence so your cash goes to the right place at the right time. Why does that matter now? Because interest rates stay painful, prices stay high, and every wrong move costs you more than it used to.

Think of it like building a house. You do not paint the walls before the foundation is set. Your money works the same way. If you chase one goal too early, you can leave yourself exposed when life hits hard. The goal here is not perfection. It is order.

What to focus on first

- Cover the basics first. Keep housing, food, utilities, and transportation stable.

- Protect yourself from shocks. Start a small emergency fund before attacking extra debt.

- Grab free money. Get the full employer 401(k) match if you have one.

- Kill toxic debt next. High-interest credit card debt can drain your progress fast.

- Then split your extra cash. Put money toward investing, larger savings goals, and any remaining debt.

What is the financial order of operations?

The financial order of operations is a step-by-step way to decide where your money goes. It helps you answer one question: what gives you the best next move, not just the most emotionally satisfying one?

Dave Ramsey has his debt snowball. The 50/30/20 budget has its split. This is different. The financial order of operations is about sequence. You build stability first, then momentum, then growth. That order matters because a mistake at the wrong step can wipe out months of progress.

Priority is a filter. If every dollar has a job, the job should match the stage of your finances, not your mood.

How the financial order of operations works

Start with survival. If your rent is shaky or your groceries are going on a card every week, stop talking about index funds for a second. Get your basics under control. After that, build a small emergency fund, usually $500 to $1,000, so a flat tire does not turn into a 22% APR disaster.

Then take the free match if your employer offers one. That is instant return. Skipping it is like leaving cash on the table because you forgot to pick it up. After that, move to high-interest debt. Credit card balances, personal loans, and payday debt can all outrun most safe investments.

Once the bleeding slows, you can increase your emergency fund, invest more, and push extra dollars toward medium-term goals. That might mean a house down payment, tuition, or a bigger cash buffer. But the order stays the same. Foundation first. Growth second.

Step 1: Stabilize your monthly cash flow

Before anything else, make sure your income covers your essentials. If it does not, the answer may be extra hours, a side gig, a cheaper phone plan, or a room change. Not glamorous. But it works.

This step is about stopping financial leaks. Are you paying late fees? Using buy now, pay later for routine purchases? Running your checking account to zero every month? Fix those issues first.

Step 2: Build a starter emergency fund

A starter emergency fund keeps small problems from becoming expensive ones. The Federal Reserve has reported that many households would struggle to cover a modest emergency expense out of pocket. That is exactly why this step comes early.

Keep this money in a plain savings account, not in stocks. You want speed and certainty, not upside. Think of it as a spare tire, not a performance upgrade.

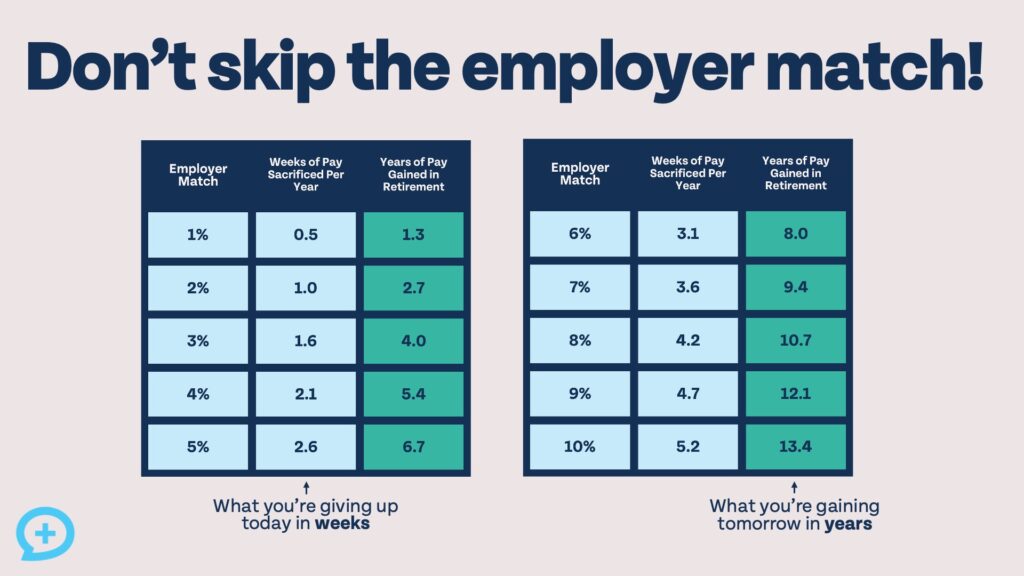

Step 3: Take any employer match

If your employer matches part of your 401(k) contribution, get enough to claim the full match. That match is part of your pay. Ignoring it lowers your compensation.

Some people want to wipe out all debt before investing. That can make sense if your debt is crushing you. But if you pass up a match, you are giving away guaranteed value while paying your full bills. That trade rarely holds up.

Where debt fits in the financial order of operations

Debt is where many people get tangled. Not all debt deserves the same treatment. A low-rate mortgage is not the same thing as a credit card balance at 28%. Treat them differently.

High-interest debt should move to the front of the line. The reason is simple. The math is brutal. A balance that charges you a steep rate can beat most long-term investment returns, especially after tax and fees. Paying it down is a guaranteed, risk-free return equal to the interest rate you avoid.

But do not drain every savings account to erase every debt dollar if that leaves you exposed. What happens if your car dies next week? Then you are back in debt, and now you have no cushion. Balance matters.

Good debt versus bad debt

Good debt is a loaded phrase, so use it carefully. A mortgage with a manageable payment and a clear plan can support your long-term finances. Student loans may do the same, depending on rate and repayment terms. Credit card debt usually does not belong in that category.

Look at the rate, the payment, and the risk. That three-part check is more useful than any label.

How to decide between saving, investing, and debt payoff

This is where people overcomplicate things. They think every extra dollar needs a perfect home. It does not. You need a rule that fits your stage.

- If you lack a starter emergency fund, build that first.

- If your employer offers a match, take it while contributing enough to get it.

- If you carry high-interest debt, direct extra money there.

- If your debt is under control, increase retirement contributions and larger savings goals.

That sequence is simple, but simple is not weak. It keeps you from trying to do everything at once and doing none of it well.

Here is the thing. The best order is the one you can stick with for months, not the one that sounds smartest on paper.

Common mistakes that wreck the plan

One mistake is keeping too little cash on hand. People hate idle money, so they throw every spare dollar at debt. Then the car repair hits. The credit card comes back out, and the cycle starts again.

Another mistake is delaying retirement too long. If you are young and your employer matches contributions, waiting years to invest can cost you real money. Time is a force multiplier. Miss enough of it and the gap gets ugly.

And do not ignore fees and rates. A 3% balance transfer fee, a high annual fee, or a dragged-out loan term can change the math fast. Read the actual numbers, not the marketing pitch. Would you run a race while wearing boots?

A simple way to put this into action

Set one weekly money check-in. Ten minutes is enough. Review your checking balance, next bill due, savings target, and debt payment. That habit keeps the order in front of you instead of buried in a spreadsheet.

Then automate the first priorities. Send your emergency fund transfer on payday. Set retirement contributions to at least the match. Put extra debt payments on autopilot if your budget can handle it. Automation turns discipline into plumbing.

If you only change one thing this month, change the order of your next dollar. That is where the real win starts.

What to do next

Use the financial order of operations as a pressure test for every money choice you make. If a move helps your current stage, keep it. If it jumps ahead of the basics, slow down and rethink it.

The market will keep offering noise. Your job is to keep your sequence clean. What happens when your next extra $500 knows exactly where to go?