How Bank Bonus Taxes Work

Bank account bonuses look like easy money until tax season turns that free cash into a smaller payday. If you are opening checking or savings accounts for extra rewards, you need to understand bank bonus taxes before you stack too many offers. Most banks treat these bonuses as taxable income, and that can change the real value of a deal fast. A $300 signup offer is not always worth $300 in your pocket once federal income tax enters the picture. And if you earn several bonuses in one year, the paperwork can pile up. That matters now because banks keep pushing signup offers, rates are shifting, and more people are chasing short-term returns. The smart move is simple. Know how the IRS usually treats account bonuses, know which tax forms may show up, and know how to judge whether the offer still makes sense after taxes.

What to know before you sign up

- Most bank bonuses count as taxable income, usually reported on a 1099 form.

- The tax hit depends on your bracket, so the same $200 bonus is worth different amounts to different people.

- Interest and bonuses are often reported differently, even if both come from the same bank.

- You should compare the after-tax value of a bonus against fees, deposit rules, and better savings options.

Are bank bonus taxes real? Yes, and the IRS usually treats them as income

Yes. In most cases, bank signup bonuses are taxable.

Banks often report cash bonuses tied to opening a checking or savings account as interest income or miscellaneous income, depending on how the offer is structured. The exact form can vary, but the broad tax result usually does not. You received money from the bank, and the IRS wants its cut.

According to the IRS and tax reporting rules banks follow, deposit account bonuses often show up on Form 1099-INT if they are tied to your account relationship. Some banks may use Form 1099-MISC in certain cases. Either way, you should expect the bonus to be taxable unless the terms clearly say otherwise.

Free money from a bank is rarely free after taxes. Treat every bonus like income the day you earn it.

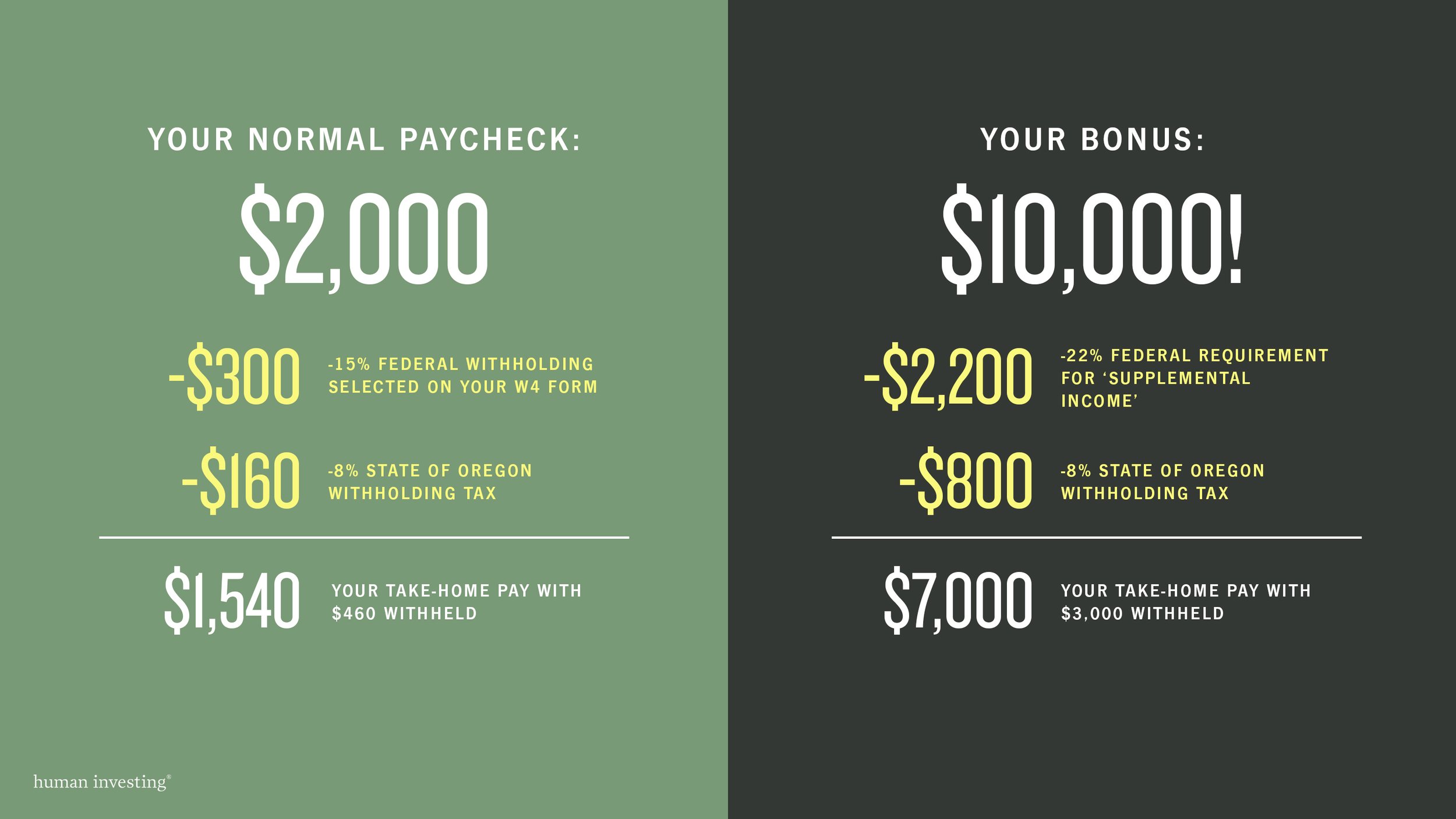

How bank bonus taxes affect the real value of an offer

This is where people get sloppy. They see the headline number and stop there.

Say a bank offers a $400 bonus for opening a checking account, setting up direct deposit, and keeping the account open for 90 days. If you are in the 22% federal tax bracket, that $400 bonus may net about $312 after federal income tax, before any state taxes. If your state taxes income too, your take-home drops more.

Here is a quick way to think about it:

- Start with the bonus amount.

- Estimate your federal tax rate.

- Add your state tax rate if it applies.

- Subtract any monthly maintenance fees or opportunity cost from parked cash.

What is the real lesson? A flashy bonus can shrink fast, a bit like a restaurant bill after tax and tip. The menu price is not the final number.

Which tax forms show up for bank bonus taxes?

You will usually see one of two forms.

1099-INT

This is common when the bank treats the bonus like interest. If you earned at least $10 in reportable interest, including certain bonuses, the bank may send Form 1099-INT. That form is also used for regular savings account interest, CDs, and some other deposit earnings.

1099-MISC

Some promotions may be reported on Form 1099-MISC instead. This can happen when the reward is not framed as interest on a deposit account. The reporting path can differ by institution and by the structure of the offer.

Look, the form matters for recordkeeping, but not for the main question. If the bank reports the payment as income, you need to deal with it on your tax return.

When do banks send tax forms for bank bonus taxes?

Banks generally send 1099 forms by January 31 for the prior tax year. If you earned a bonus in 2024, you would usually expect the form in early 2025. Delivery may happen by mail or through your online account portal.

Do not assume no form means no tax. You are still responsible for reporting taxable income even if a form gets lost, arrives late, or never shows up. Honestly, this is where bonus chasers get burned. They close an account, forget about the reward, and then miss the reporting.

How to track bank bonus taxes without making it a mess

If you open multiple accounts, tracking matters. A lot.

Use a simple spreadsheet with the bank name, bonus amount, date earned, expected tax form, and any fees paid. Add the direct deposit requirement, minimum balance rule, and account closing date too. That last part saves you from early closure fees and from forgetting where the money came from.

A clean tracking system works like keeping a kitchen mise en place. Everything is visible, and nothing gets left behind when it is time to finish the dish.

How to judge whether a bank bonus is worth it after taxes

Some are worth the effort. Some are junk in nice packaging.

Ask these questions before you apply:

- What is the after-tax value of the bonus?

- How much money must you deposit or keep idle?

- Are there monthly fees?

- Does the bank require direct deposit, debit card use, or bill pay activity?

- Could your cash earn more in a high-yield savings account, money market account, or Treasury bill during the same period?

If a $250 bonus requires parking $15,000 for four months, the deal may be weaker than it looks, especially if rates elsewhere are strong. But a $300 checking bonus tied to payroll deposits and no long lockup can still be a solid move.

Common mistakes people make with bank bonus taxes

Ignoring state taxes

Federal tax gets most of the attention, but state income tax can reduce the value further.

Forgetting fees

A monthly maintenance fee can eat a bonus from the inside out. Read the waiver rules before you open the account.

Confusing credit card bonuses with bank account bonuses

Credit card rewards are often treated differently when tied to spending. Bank deposit bonuses usually do not get the same treatment. They are separate animals.

Not setting aside cash for taxes

If you stack several offers, set aside part of each payout for tax season. Even a rough reserve helps.

What the source gets right, and what readers should keep in mind

The Money Crashers piece correctly points readers toward the core issue. Bank bonuses are often taxable, and the reporting can come through a 1099. That is the part many promo hunters miss because the signup page focuses on the reward, not the aftermath.

But here is the thing. The tax label is only part of the decision. You should also measure time, cash lockup, fees, and the chance that you forget one of the qualification steps (banks count on that, by the way). Missing a direct deposit window or balance target can turn a good offer into wasted effort.

A smarter way to approach bank bonus taxes

Go after offers with simple terms, low fees, and a strong after-tax payout. Keep records. Check your 1099 forms early. And if you are opening accounts at scale, treat it like a side hustle, not a lucky coupon.

The next time a bank waves a $200 or $500 offer in front of you, do one quick calculation before you click. After taxes, is the bonus still good enough to earn your attention?