Index Funds: A Simple Stock Investing Strategy

If you want to invest in stocks without spending your nights tracking earnings calls and market rumors, index funds are hard to ignore. They give you instant spread across hundreds or thousands of companies, and they usually cost far less than actively managed funds. That matters because fees, taxes, and bad timing can quietly eat your returns for years.

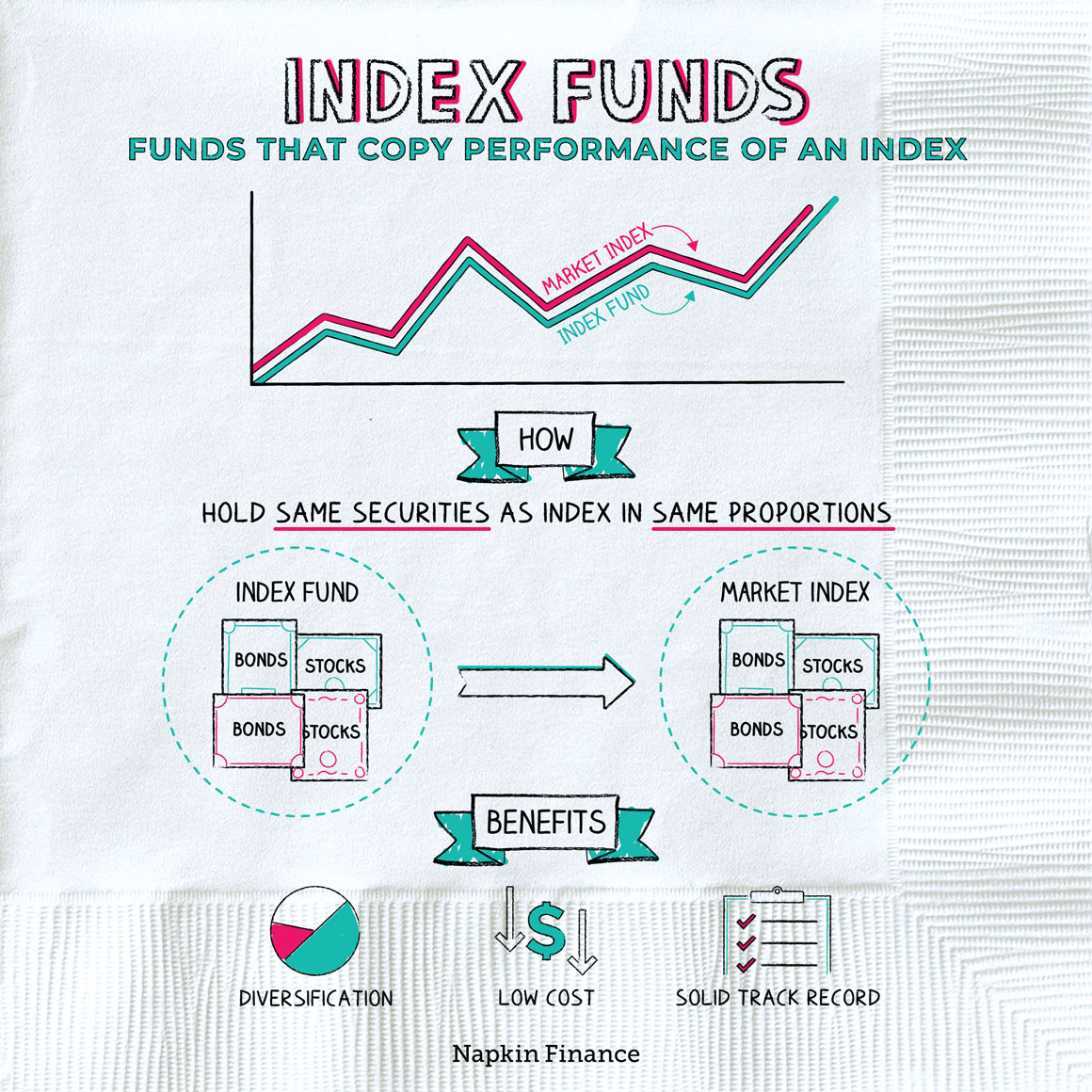

Look, most people do not lose money because the stock market is broken. They lose money because they overtrade, chase performance, or pay too much for help they do not need. Index funds cut through that noise. They are built to match a market benchmark, such as the S&P 500, rather than try to beat it (which is where many fund managers stumble).

So what does that mean for you? Less guesswork. Fewer moving parts. And a portfolio that can behave like a well-built house instead of a stack of chairs.

- Low costs matter. Expense ratios can have a long-term drag on returns.

- Diversification is built in. One fund can hold many stocks across sectors.

- They fit buy-and-hold investors. You do not need to trade often.

- They are easy to compare. You can screen funds by index, fee, and tracking error.

What are index funds in stock investing?

An index fund is a mutual fund or ETF designed to track a market index. That index might be the S&P 500, the Total Stock Market Index, or a sector index such as technology or healthcare. The fund does not try to beat the market. It tries to mirror it.

That passive approach changes the job. Instead of paying a manager to pick winners, you are buying the market itself. And because the fund changes holdings only when the index changes, trading costs often stay lower than in active funds.

Index funds are a rules-based way to own stocks. You are buying the market’s average, minus a small fee, instead of betting on a manager’s skill.

Why index funds often beat stock picking

Active stock picking sounds appealing. Who would not want to buy the next big winner? But the evidence has been stubborn for decades. Standard & Poor’s SPIVA scorecards regularly show that most actively managed U.S. stock funds underperform their benchmarks over long periods, especially after fees.

The reason is plain. Markets already price in a lot of public information. Beating that crowd is tough, and the costs of trying can pile up fast. If you buy a fund with a 1% expense ratio and the index version costs 0.03%, that gap can become seismic over 20 years. Why hand over return after return if you do not need to?

There is another edge too. Index funds reduce the risk of one bad pick wrecking your plan. If one company fails, it barely dents the basket. That is a far calmer setup than trying to nail a handful of stocks on your own.

How to choose an index fund for your portfolio

Start with your goal. Are you building long-term growth, income, or a simple retirement portfolio? The answer should shape the index you choose. A broad market fund works for many investors because it covers a wide slice of U.S. stocks without asking you to guess which sector will lead next.

Then check the basics. Keep your eye on fees, the index being tracked, fund size, and how closely the fund follows its benchmark. A tiny expense ratio is good, but it is not the whole story. You also want a fund with solid liquidity and low tracking error.

- Pick the index. Broad U.S. market, large-cap, small-cap, or international.

- Compare costs. Lower expense ratios usually help more over time.

- Check holdings. Make sure you understand what the fund actually owns.

- Review taxes. ETFs can be more tax efficient than mutual funds in taxable accounts.

- Match the fund to your plan. Do not buy a fund just because it is popular.

ETFs vs. mutual funds

Both can be index funds. ETFs trade during market hours like stocks, while mutual funds are priced once per day. ETFs often have a tax edge in taxable accounts because of how they handle redemptions. Mutual funds can still work well inside retirement accounts, especially if you want automatic investing.

Think of it like buying groceries. An ETF is the grab-and-go option. A mutual fund is the prepacked basket. The food can be similar, but the checkout process is different.

What risks do index funds still carry?

Index funds are simple, but they are not magic. If the market drops, your fund drops too. If you own a fund tied to the S&P 500, you still hold large U.S. companies, and that means you are exposed to the same broad market swings everyone else feels.

There is also concentration risk. Many investors think they are diversified because they own an index fund, but some indexes lean heavily on a few giant names. That matters. A fund tracking a market-cap weighted index can become less balanced than you expect.

And there is one more trap. People sometimes buy an index fund and then panic-sell during a downturn. The fund did its job. The investor did not. That gap is where many portfolios get hurt.

How to use index funds in a real plan

For many investors, a three-fund setup is enough. One U.S. stock index fund, one international stock index fund, and one bond fund can cover a lot of ground without creating a mess. You can tilt more aggressive or more conservative depending on your age, income, and risk tolerance.

Rebalance once or twice a year. That keeps your target mix from drifting too far. And if you invest from each paycheck, automate it. Consistency beats clever timing more often than people want to admit.

Here is the part that often gets missed: index funds are not a shortcut around discipline. They are a cleaner tool for disciplined investing. Use them that way, and they can save you time, money, and a lot of second-guessing.

A better stock investing default

If you want a stock strategy that is easy to explain, hard to misuse, and inexpensive to run, index funds belong near the top of the list. They will not make you feel brilliant every quarter. That is the point.

Ask yourself one question before you buy a stock tip or a hot fund: do you want to own the market, or do you want to keep chasing it?