Standard Tax Deduction vs Itemizing: How to Choose

Picking between the standard tax deduction and itemizing can change your tax bill in a real way. If you choose the wrong one, you leave money on the table. If you choose the right one, you keep more of what you earned, and that matters now because tax rules shift, income is tight for many households, and a small mistake can mean paying more than you need to. The standard tax deduction is the default for most filers, but itemizing still wins for some people with high mortgage interest, large medical bills, or major charitable giving. So how do you know which path fits your return?

Look at the numbers, not the habit. That is the whole game.

What to know about the standard tax deduction

The standard tax deduction is a fixed amount that reduces your taxable income. The IRS sets it each year, and the amount depends on your filing status, age, and whether you are blind. For many taxpayers, this is the simplest route because you do not need to track every deductible expense.

For 2024 returns filed in 2025, the standard deduction is $14,600 for single filers and married people filing separately, $29,200 for married couples filing jointly, and $21,900 for heads of household, according to the IRS. Those numbers move with inflation, so check the current year before you file.

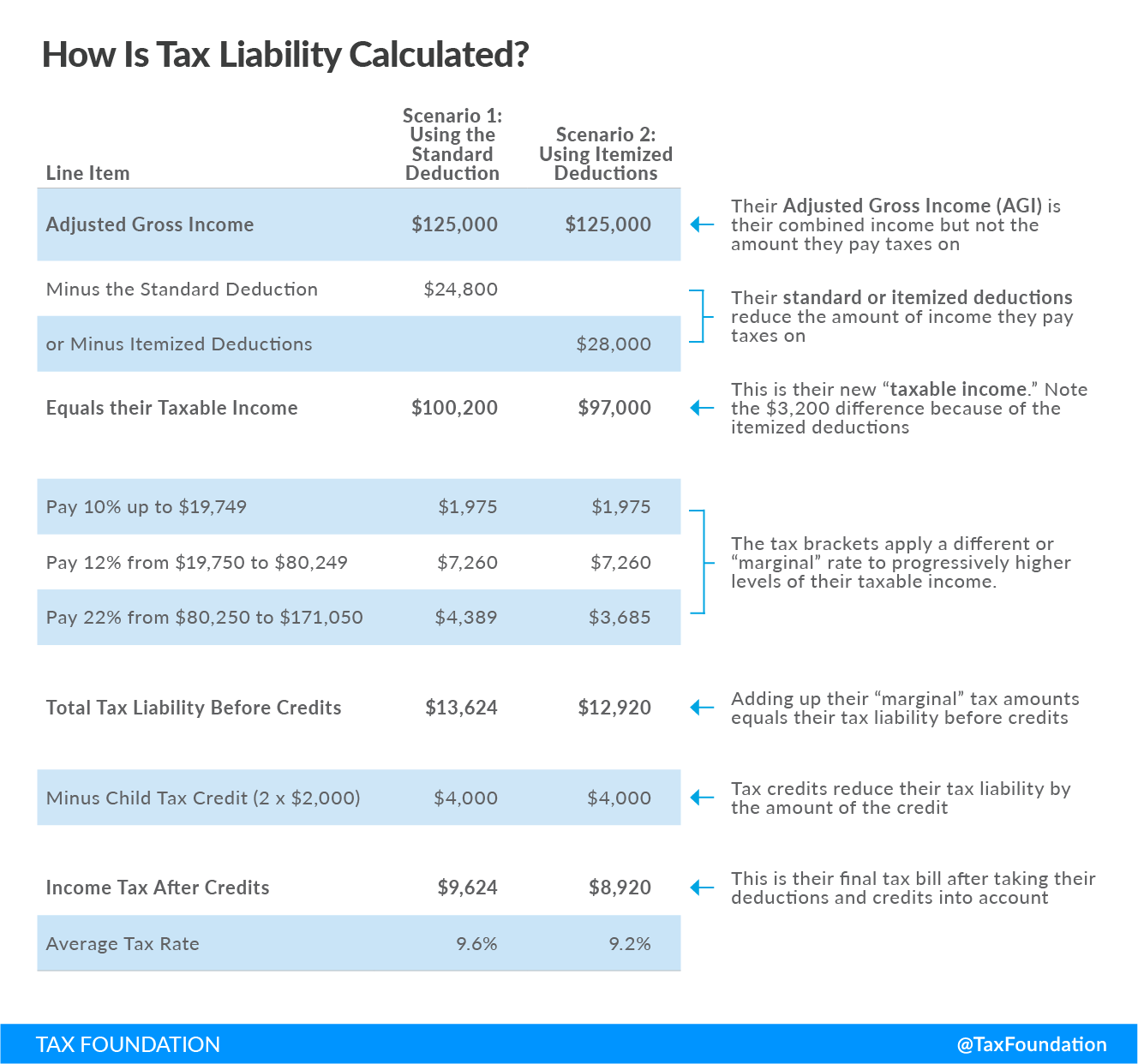

Big idea: If your itemized deductions do not beat your standard deduction, you should usually take the standard deduction. Tax software makes this comparison easy, but the decision is still yours.

When itemizing beats the standard tax deduction

Itemizing means listing eligible deductions on Schedule A instead of taking the flat standard amount. This usually makes sense only when your deductible expenses are high enough to clear the standard deduction threshold. Think of it like choosing between a flat-rate fare and a metered ride. If your trip is long, the meter can win. If not, the flat rate is cleaner and cheaper.

Common itemized deductions include mortgage interest, state and local taxes up to the federal cap, charitable donations, and certain medical expenses above a set percentage of your adjusted gross income. Homeowners in high-cost areas, people with big medical bills, and generous donors are the usual candidates.

Main expenses that can justify itemizing

- Mortgage interest on eligible home loans

- State and local taxes, including income or sales tax, plus property tax, subject to the federal limit

- Charitable contributions to qualified organizations

- Medical and dental expenses above the IRS threshold based on adjusted gross income

- Casualty and theft losses in limited cases tied to federal disaster rules

How to compare the standard tax deduction with itemizing

Do the math before you decide. Add up your possible itemized deductions, then compare that total to your standard deduction. If itemizing comes in lower, stop there and take the standard deduction. If it is higher, itemizing may save you tax.

- Gather mortgage interest statements, property tax records, donation receipts, and medical expense totals.

- Check the current standard deduction for your filing status.

- Compare both totals with the same tax year in mind.

- Run the numbers in tax software or with a tax pro if your situation is messy.

Here is the part people miss. Some deductions only matter if you can document them well. A charity receipt in a drawer does not help if you cannot prove the gift. Tax prep is part math, part paperwork. Annoying? Yes. Non-negotiable? Also yes.

Common mistakes with the standard tax deduction

People make the same mistakes over and over. They assume itemizing is always better because they own a home. Not true. They also forget that the standard deduction can be the best deal even when they have some deductible expenses.

Another error is double-counting or guessing at expenses. That can lead to problems if the IRS asks for proof. A clean return beats a shaky one. Every time.

And one more thing. Some taxpayers overlook above-the-line deductions, like certain IRA contributions or HSA contributions, because they focus only on the standard deduction versus itemizing choice. Those are separate issues, and they can affect your final tax picture.

Who should pay extra attention to the standard tax deduction?

Renters often take the standard deduction because they usually have fewer itemized deductions. New homeowners can go either way, depending on mortgage interest and property taxes. Retirees should check medical expenses and charitable giving closely, since those can push itemized totals upward.

Self-employed people are in a different lane. Business deductions do not go on Schedule A, so they should not confuse business write-offs with itemized personal deductions. That mix-up causes real filing errors.

Ask yourself one simple question. If you stripped away the mortgage and the donations, would your itemized total still beat the standard deduction?

Where the standard tax deduction fits in your tax plan

The standard deduction is not a consolation prize. For millions of households, it is the smartest choice because it saves time and cuts the risk of mistakes. The IRS data and tax filing patterns both point the same way. Most taxpayers do not itemize.

Still, you should review your numbers every year. Life changes. A home purchase, a surge in medical costs, or a larger giving year can shift the math fast. Treat this like checking your tire pressure before a long drive. Small checks prevent bigger problems later.

A cleaner way to file next year

Build a simple tax folder now. Put mortgage statements, donation receipts, property tax bills, and medical expense records in one place as the year goes on. That way, when tax season hits, you can compare the standard tax deduction against itemizing without scrambling.

That habit takes less than ten minutes a month, and it can save you far more than that in tax savings. Why guess when the answer is usually sitting in your paperwork?