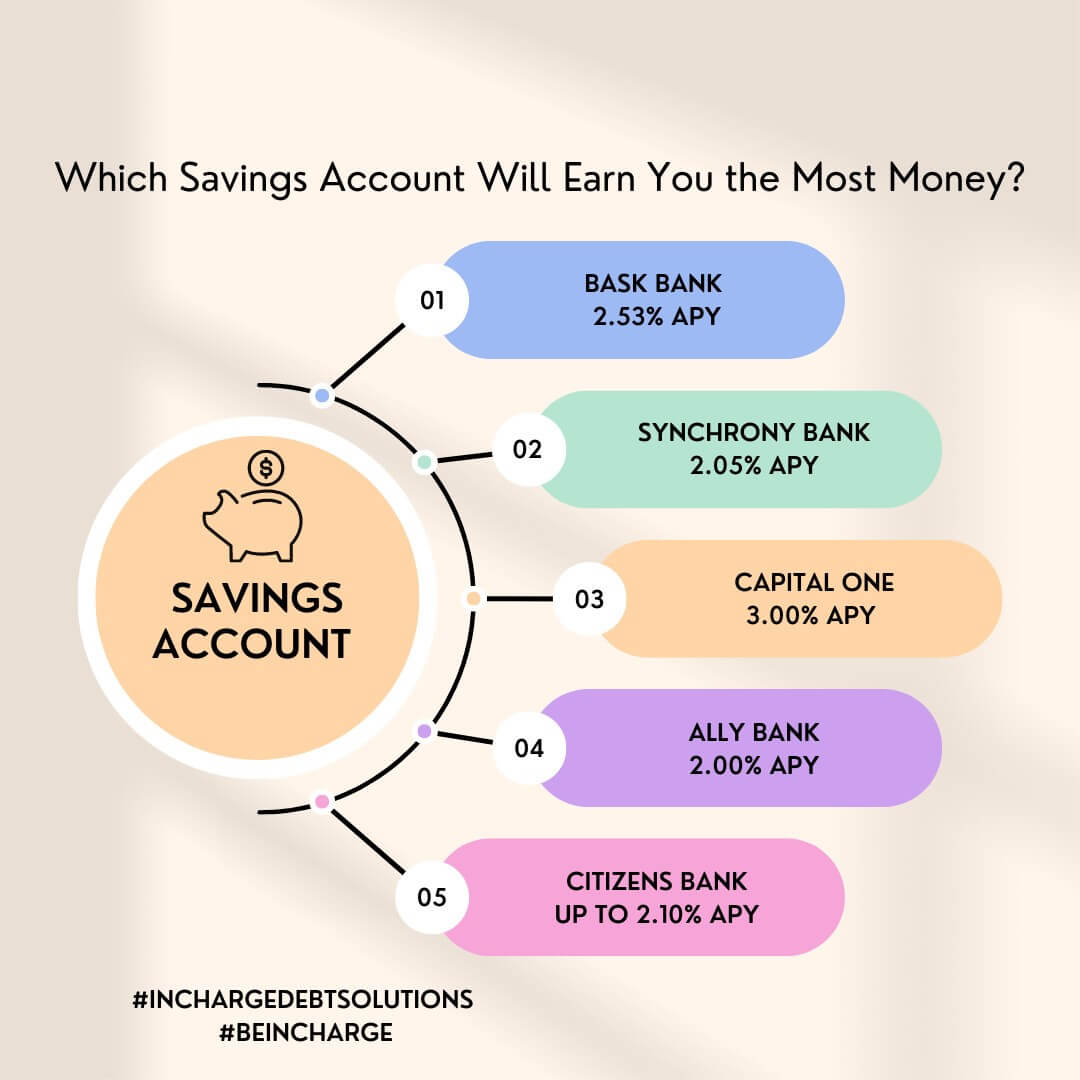

Best High-Yield Savings Accounts for Your Cash

If your savings still sit in a traditional bank account earning next to nothing, you are giving up easy money. A best high-yield savings account can pay several times more interest than many brick-and-mortar options, which matters if you are building an emergency fund, parking home down payment money, or just trying to keep cash productive while rates remain elevated. But rate alone is not the whole story. Some accounts look great on a comparison table, then bury limits in transfer rules, balance requirements, or clunky mobile tools. That is where people get tripped up. You need an account that pays a strong annual percentage yield, keeps fees at zero, and lets you move your money without friction. That sounds basic. It is also non-negotiable.

What matters most

- APY is the headline, but fees and transfer limits can wipe out part of the gain.

- FDIC or NCUA insurance should be a baseline requirement, not a bonus.

- The best high-yield savings account for you depends on how fast you need access to cash.

- Digital experience counts, especially if you move money often or manage multiple savings goals.

How to judge the best high-yield savings account

Start with APY, because that is the direct return on your cash. As Money Crashers notes in its roundup of top accounts, online banks and fintech-backed options often lead the market on yield because they run with lower overhead than branch-heavy banks. That cost edge gets passed to depositors, at least part of the time.

But a high rate can distract you from the fine print. Look at minimum opening deposits, minimum balance rules, excess withdrawal policies, linked account transfer speed, and whether the bank has a track record of keeping rates competitive after the promo shine fades. Think of it like buying a solid kitchen knife. Sharpness matters, sure, but balance and grip matter too.

And yes, customer support matters.

Core filters to use

- Insurance coverage

Check for FDIC insurance at banks or NCUA insurance at credit unions. Coverage typically protects up to applicable legal limits per depositor, per institution, per ownership category. - No monthly maintenance fee

There is little reason to accept one in this category. Too many good accounts charge nothing. - Competitive APY without hoops

Be wary of accounts that require direct deposit, debit card swipes, or a checking bundle just to earn the top rate. - Fast transfers

An emergency fund is no help if moving cash feels like mailing a paper check in 2006. - Usable mobile app and web access

Honestly, this is where some banks still fall apart.

Why the best high-yield savings accounts beat traditional banks

Large legacy banks still offer savings rates that can barely register, even when the Federal Reserve has pushed short-term rates higher. That spread is not an accident. Big banks know many customers stay put for convenience, direct deposit ties, and simple inertia.

Online savings accounts pressure that model. They compete harder on yield because deposit gathering is the product. If one account pays 4.50% APY and another pays 0.01%, the gap on a $10,000 balance is massive over a year. Even after rate moves, the principle holds. Idle cash should earn something real.

Chasing every last basis point is not always worth it. Moving from a weak bank rate to a strong online rate usually is.

Best high-yield savings account features to compare before you open one

What should you compare first? Here is the short list I would use after years of watching banks sell simplicity while hiding friction in the details.

1. APY and rate history

A top-tier APY gets your attention, but rate history tells you how the bank behaves. Some institutions stay near the top of the market. Others pop up with flashy yields, then slide down fast once they have enough deposits.

2. Access to your money

Check ACH transfer timing, mobile check deposit, wire availability, and ATM access if offered. If this account holds your emergency fund, speed matters more than tiny APY differences.

3. Fees and account minimums

The cleanest setup is simple. No monthly fee, no minimum balance requirement, and no minimum deposit beyond a modest opening threshold.

4. Linked products

Some banks make life easier if you also use their checking account, CD, or cash management account. That can be useful. But do not let a bundle talk you into a weaker savings rate.

5. Customer experience

Read recent reviews with caution, then look for patterns. Repeated complaints about frozen transfers, identity verification delays, or poor support are a real signal.

Who should open the best high-yield savings account?

These accounts work best for money you may need within the next few months or years. Emergency funds. Travel savings. Tax reserves for freelancers. A car fund. A house down payment that is too near-term for stock market risk.

They are not ideal for long-term retirement investing. If your time horizon is a decade or more, a tax-advantaged brokerage or retirement account usually gives you better growth odds, though with market volatility. Different tools, different jobs.

Good use cases

- Emergency fund with three to six months of expenses

- Short-term savings goals under five years

- Cash you are holding while waiting to pay taxes or tuition

- Money you want safe, liquid, and earning more than a standard savings account

Common mistakes people make with high-yield savings accounts

The biggest mistake is focusing only on the number at the top of the page. A slightly lower APY at a bank with faster transfers, cleaner support, and no nonsense may be the better choice for your real life.

Another mistake is forgetting taxes. Interest earned in a savings account is generally taxable in the year you receive it, so your after-tax return may be lower than the APY suggests. That does not make the account a bad deal. It just means you should plan with clear eyes.

But here is the one that really stings. People move cash into a better account, then keep too much sitting in checking earning zero because they never set up automatic transfers.

How to pick the best high-yield savings account for your goals

If you want a practical way to choose, keep it simple.

- Define the job

Is this account for emergencies, a sinking fund, or a near-term purchase? - Set your access needs

If you may need same-week cash, prioritize transfer speed and linked checking options. - Compare the real terms

Review APY, fees, minimums, and support channels side by side. - Automate deposits

Even a great account fails if you do not feed it. - Recheck rates a few times a year

You do not need to micromanage, but you should not ignore drift either.

(And if opening the account takes more than a few minutes to understand, that is a hint.)

What Money Crashers gets right about the best high-yield savings accounts

The Money Crashers list is useful because it frames high-yield savings accounts as a category with tradeoffs, not as a single winner-take-all race. That is the right lens. The strongest options tend to share a few traits, including competitive yields, low or no fees, and easy online access. Their roundup helps narrow the field, especially if you want a quick sense of which banks are offering strong rates now.

Still, no roundup can choose for you. Your best fit depends on whether you value maximum yield, branch access, customer service, or speed of movement between accounts. Are you opening one account for a rainy day fund, or building a whole cash system with buckets and automation?

A smarter next move

The gap between a weak savings account and the best high-yield savings account is one of the easiest wins in personal finance. There is no stock picking, no budget overhaul, and no heroic discipline required. You just move your cash to a better shelf.

So check your current APY today. If it looks anemic, compare a few top options from the Money Crashers list, read the fee page, test the mobile app, and set up recurring transfers. Rates will change. The habit of making your cash work harder should not.