Budgeting for Irregular Income

If your paycheck changes from month to month, planning can feel like guesswork. One month looks fine. The next one gets tight fast. That is why budgeting for irregular income matters right now. Rising housing, food, and insurance costs leave less room for mistakes, and uneven cash flow makes every bill harder to time. I have covered personal finance long enough to know this problem gets brushed off with weak advice like “just save more.” That is not enough. You need a system that works when income swings, whether you freelance, earn commissions, drive gig apps, or run a small business. The good news is simple. You can build a budget that protects essentials first, smooths out uneven pay, and helps you stop making money decisions in panic mode.

What to do first

- Base your budget on your lowest reliable income month, not your best one.

- Separate essentials from flexible spending so cuts are obvious when pay drops.

- Use a holding account or buffer to smooth cash flow across the month.

- Pay yourself on a schedule if you are self-employed or paid inconsistently.

Why budgeting for irregular income feels so hard

Most budgeting advice assumes a fixed paycheck. Yours may not work that way. Maybe your work is seasonal. Maybe shifts change. Maybe clients pay late. The result is the same. Bills arrive on schedule, but income does not.

That mismatch creates two problems. First, you may earn enough over a full year but still come up short in a single month. Second, you can fool yourself during strong months and spend as if that level will last. It often does not.

Think of irregular income like cooking on uneven heat. The food can still turn out well, but only if you stop assuming every burner runs the same way.

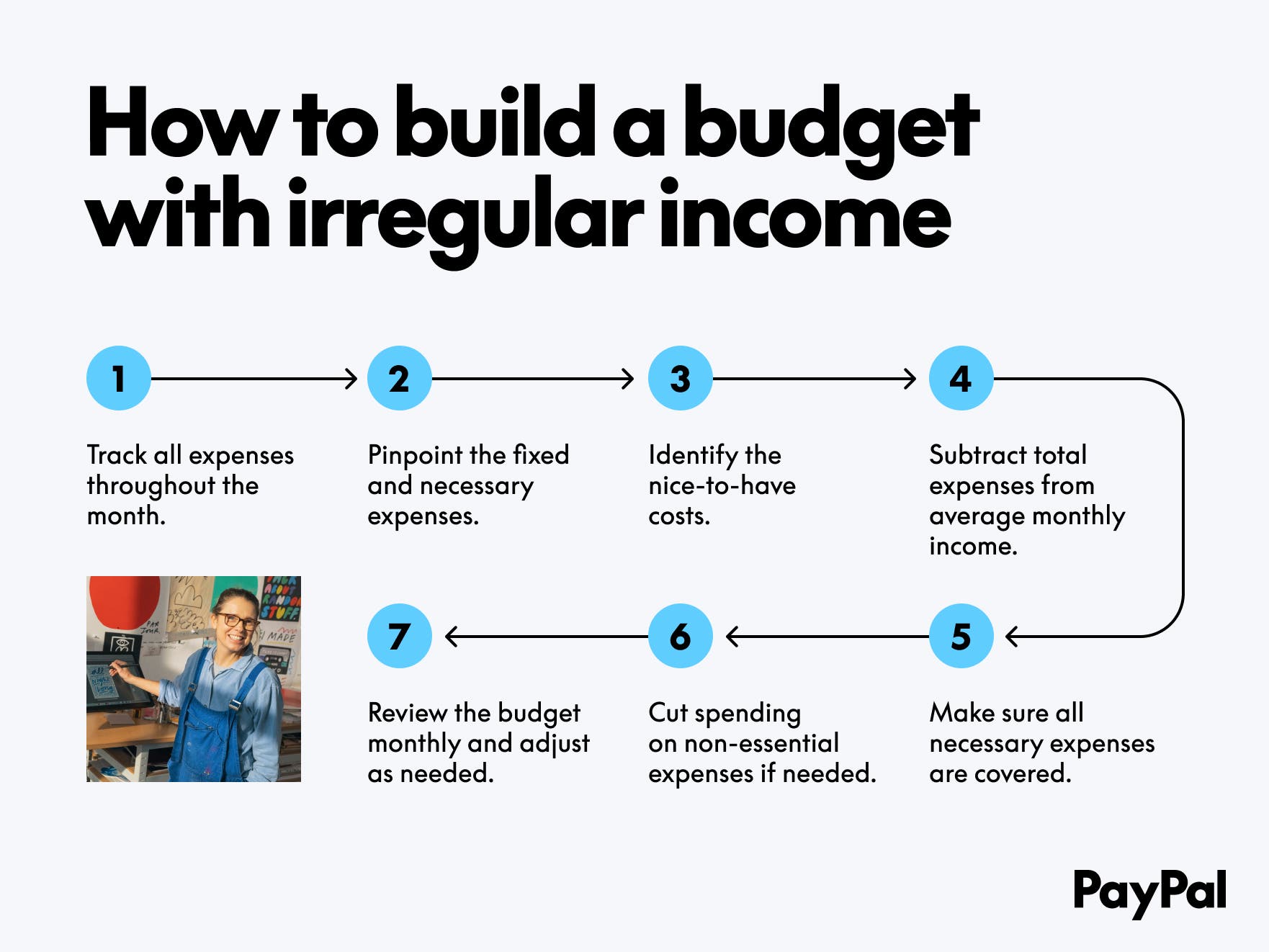

How to start budgeting for irregular income

1. Find your baseline income

Pull the last 6 to 12 months of income records. Bank deposits work. Pay stubs work. Invoice history works too. Add up what actually came in each month.

Then pick a baseline income. For most people, that should be the lowest month or a cautious average from your weakest months. Look, this is where people get too optimistic. If your monthly income ranged from $2,800 to $5,400, building your plan around $4,800 is asking for trouble.

Use the number that keeps the lights on even in a slow stretch.

2. Split expenses into two groups

You need a clean divide between bills that must get paid and spending that can move. Start with essentials:

- Rent or mortgage

- Utilities

- Groceries

- Insurance

- Transportation

- Minimum debt payments

- Child care

Then list flexible spending like eating out, shopping, subscriptions, travel, and extra debt payments. This sounds basic, but it changes how you react under pressure. Why? Because a short month stops being a full-blown crisis. It becomes a math problem.

3. Build a bare-bones budget

Your bare-bones budget covers only essentials and a few non-negotiable basics. This is your survival setting. It is the version you can run during a weak month without going into debt.

And yes, you should write this down before you need it.

Best budgeting method for irregular income

The strongest setup is usually a priority-based budget. You fund expenses in order, not all at once in theory. Money comes in. You assign it to the next most important job.

- Housing

- Utilities

- Food

- Transportation

- Insurance

- Minimum debt payments

- Core personal and family costs

- Savings buffer

- Everything else

This works better than a rigid monthly plan when income timing is messy. It also lines up with guidance from the Consumer Financial Protection Bureau, which has long advised households with variable pay to focus on income averages, bill calendars, and emergency reserves.

Use a separate buffer account

If your bank allows free savings accounts, keep one just for income smoothing. In strong months, move extra money there. In lean months, pull from it to cover the gap. That buffer acts like a shock absorber.

Honestly, this is one of the few finance habits that changes your stress level fast.

How much should your irregular income buffer be?

Start with one month of essential expenses. That is a solid first target. If your income swings hard or your industry is seasonal, push toward two to three months. According to the Federal Reserve’s recent household well-being research, many adults still struggle to cover unexpected expenses, which makes a cash buffer more than a nice idea. It is protection.

If that target feels huge, break it down:

- First goal: $500

- Next goal: half a month of essentials

- Then: one full month of essentials

Small steps count. A thin buffer is still better than starting every rough month from zero.

How to pay bills when income is uneven

Match due dates to cash flow if you can

Call service providers and ask to move due dates. Credit card issuers, utilities, and some lenders often allow this. If most of your income lands later in the month, shift bills to fit that pattern.

Use a monthly bill calendar

List every bill, amount, and due date in one place. Paper is fine. A spreadsheet is fine. An app is fine too. The point is to stop surprise withdrawals from hitting when your account is low.

Set aside taxes if you are self-employed

This one gets ignored until it hurts. Freelancers and contractors should move a percentage of each payment into a tax savings account. The IRS generally expects quarterly estimated payments for many self-employed workers. If you skip this step, a decent income month can turn into a nasty bill later.

Common mistakes in budgeting for irregular income

- Budgeting from your highest month. That is fantasy budgeting.

- Mixing business and personal spending. If you freelance or own a small business, keep them separate.

- Forgetting annual and seasonal expenses. Car repairs, holiday spending, school costs, and insurance premiums still count.

- Using credit cards as income smoothing. That is borrowing, not budgeting.

- Skipping savings during good months. Strong months should fund future weak ones.

Tools that make budgeting for irregular income easier

You do not need fancy software, but you do need visibility. A few options work well:

- Spreadsheet budget if you want full control

- Zero-based budgeting apps for assigning each dollar a job

- Separate checking and savings accounts for bills, taxes, and buffer money

- Automatic transfers to move money into savings the same day income arrives

But keep the system simple enough to use when you are tired. That matters more than features.

Budgeting for irregular income with family expenses

If other people depend on your income, your plan needs extra margin. Kids do not care that a client paid late. So raise the priority of groceries, school costs, medicine, and child care. Build those into your baseline, not your wish list.

Talk through the system with your partner or anyone sharing the budget. Decide in advance what gets cut in a weak month and what stays protected. That removes friction later. It also keeps one person from assuming the good month means open season on spending.

A family budget with variable income needs rules before stress hits, not after.

What a sample irregular income budget can look like

Say your monthly income ranges from $3,000 to $4,700. Your baseline budget might use $3,000.

- Housing: $1,100

- Utilities: $220

- Groceries: $450

- Transportation: $300

- Insurance: $250

- Minimum debt payments: $180

- Phone and internet: $150

- Child care or school costs: $200

- Buffer savings: $100

- Flexible spending: $50

If you earn $4,200 one month, the extra $1,200 does not mean you are suddenly flush. You might split it between buffer savings, taxes, sinking funds, and debt payoff. That is how uneven income becomes manageable over time.

The move that matters most next

Budgeting for irregular income is less about prediction and more about defense. You are building a system that can handle bad timing, lower months, and the occasional surprise hit. That is the real job.

Start this week. Review the last six months of income, choose your baseline number, and build your bare-bones budget around it. Then ask yourself one blunt question. If next month comes in light, do you already know which dollars cover rent, food, and gas first?

If the answer is no, that is your next fix.